Back

FiinRatings Upgrades Coteccons' Long-Term Credit Rating to BBB+ with "Stable" Outlook

On September 29, 2024, FiinRatings, a leading credit rating agency in Vietnam and a technical partner of S&P Global Ratings, upgraded Coteccons' long-term credit rating from BBB to BBB+ with a "Stable" outlook.

This recognition is a proud achievement for Coteccons after three years of restructuring and operational stabilization. The company has consistently improved its profitability, operational efficiency, and the quality of its receivables by shifting towards projects with stronger cash flows, especially FDI projects.

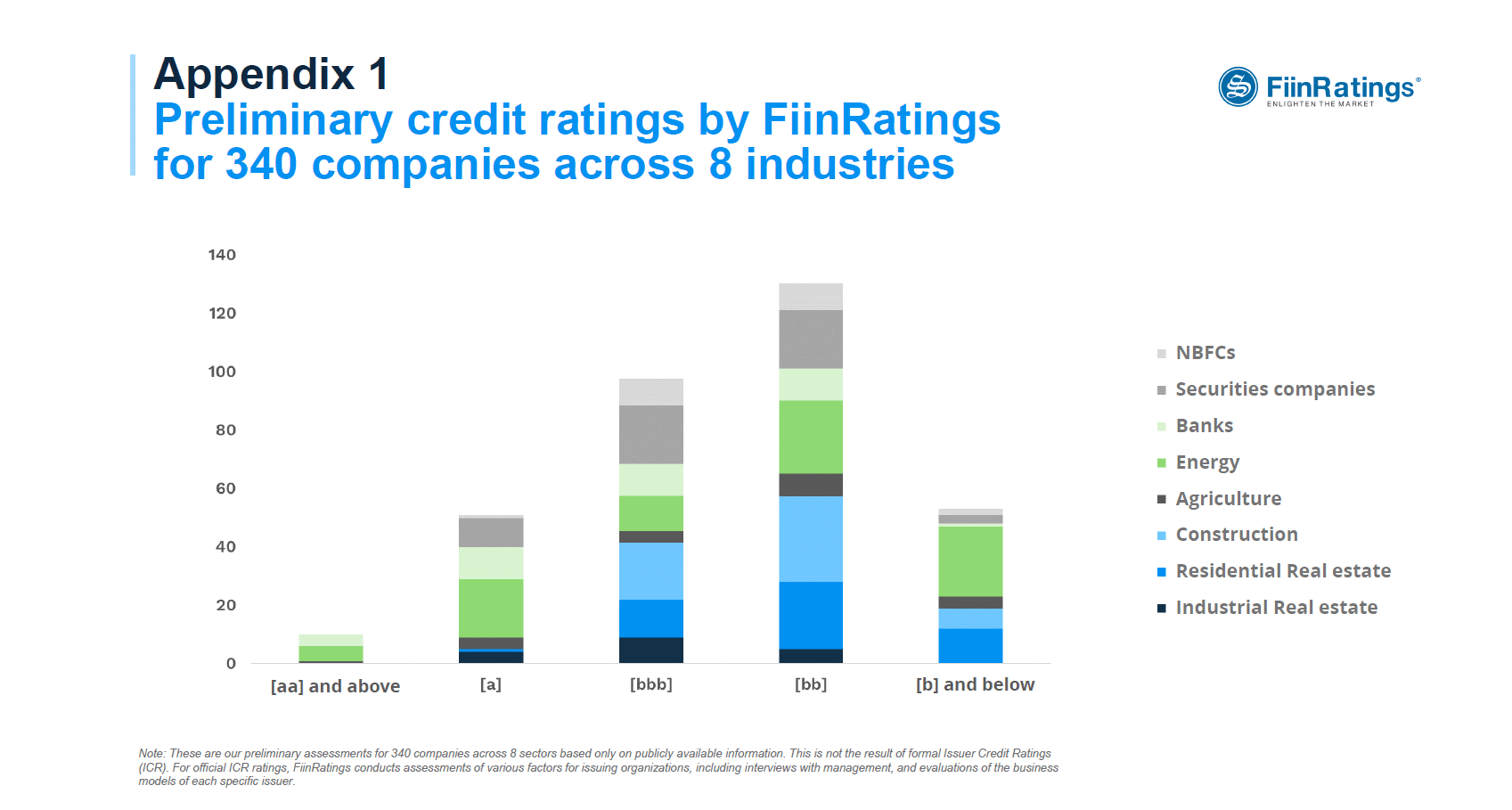

This result is particularly meaningful as the A-category ratings are typically reserved for energy companies and banks, and no construction company has ever been rated in this group. Coteccons is also the only construction company to achieve a BBB+ rating, the highest in the B-category.

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

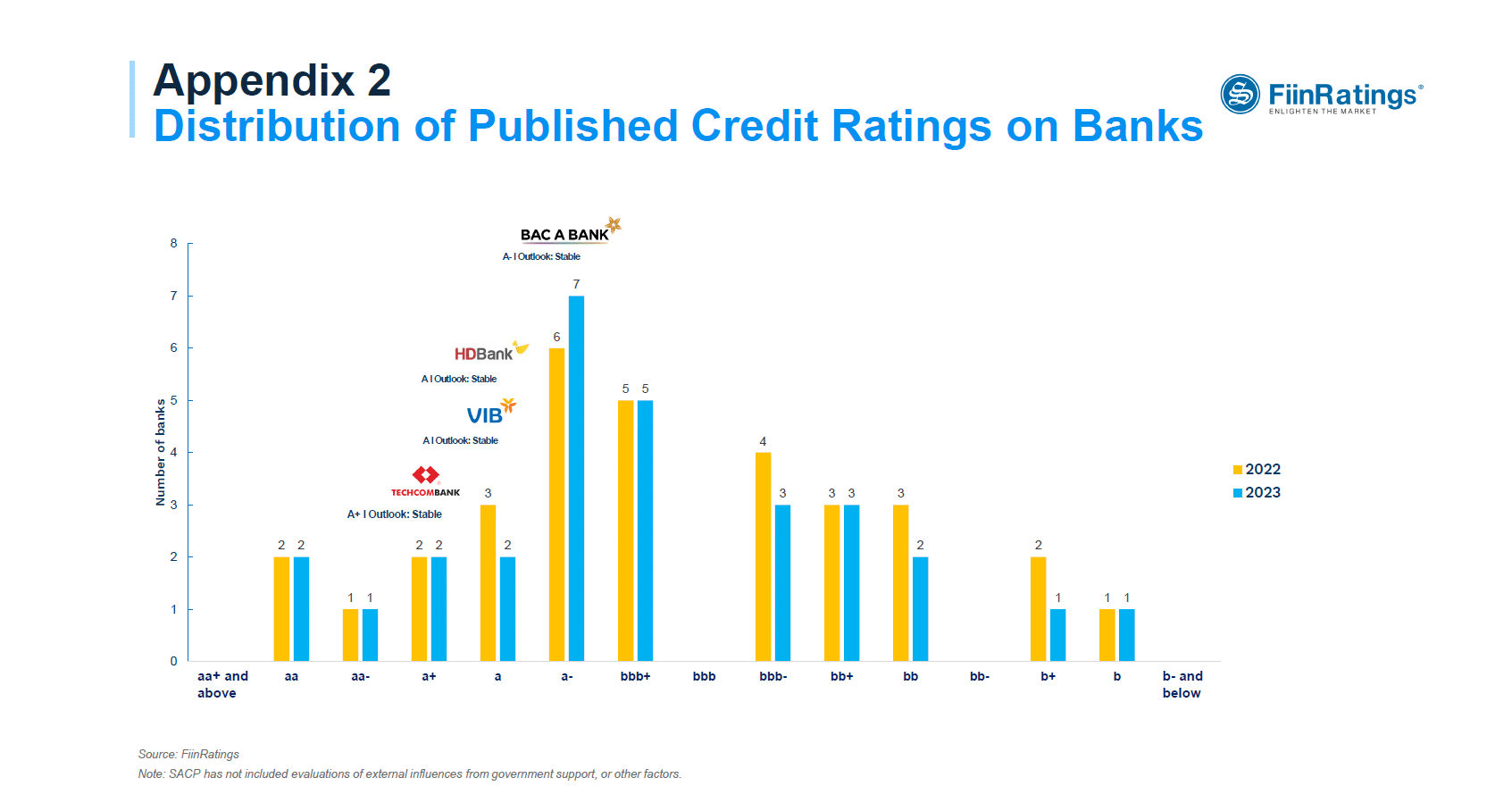

When compared to organizations in the banking sector, Coteccons' credit rating is on par with or higher than 15 credit institutions (according to 2023 data from FiinRatings).

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

When compared to organizations in the banking sector, Coteccons' credit rating is on par with or higher than 15 credit institutions (according to 2023 data from FiinRatings).

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

According to FiinRatings, "Coteccons has shown remarkable resilience in maintaining its leading position following the restructuring phase, despite the high-risk nature of the construction industry and challenging macroeconomic conditions. This resilience is reflected in its strong and sustained growth in revenue and backlog, along with notable and consistent improvements in profit margins, operational efficiency indicators and account receivables quality."

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

According to FiinRatings, "Coteccons has shown remarkable resilience in maintaining its leading position following the restructuring phase, despite the high-risk nature of the construction industry and challenging macroeconomic conditions. This resilience is reflected in its strong and sustained growth in revenue and backlog, along with notable and consistent improvements in profit margins, operational efficiency indicators and account receivables quality."

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

When compared to organizations in the banking sector, Coteccons' credit rating is on par with or higher than 15 credit institutions (according to 2023 data from FiinRatings).

Source: Vietnam Corporate Bond Market Research Report, FiinRatings

According to FiinRatings, "Coteccons has shown remarkable resilience in maintaining its leading position following the restructuring phase, despite the high-risk nature of the construction industry and challenging macroeconomic conditions. This resilience is reflected in its strong and sustained growth in revenue and backlog, along with notable and consistent improvements in profit margins, operational efficiency indicators and account receivables quality."